Step-by-Step Guide to Buying Property with a Mortgage in Portugal | A Practical Guide for Foreign Buyers

In Portugal, purchasing property with a mortgage is a common approach for many international buyers. Compared to a full cash purchase, financing involves additional steps, including bank approval, property valuation, and coordination of timelines. Understanding the structure and sequence of the process in advance can make the entire transaction much smoother.

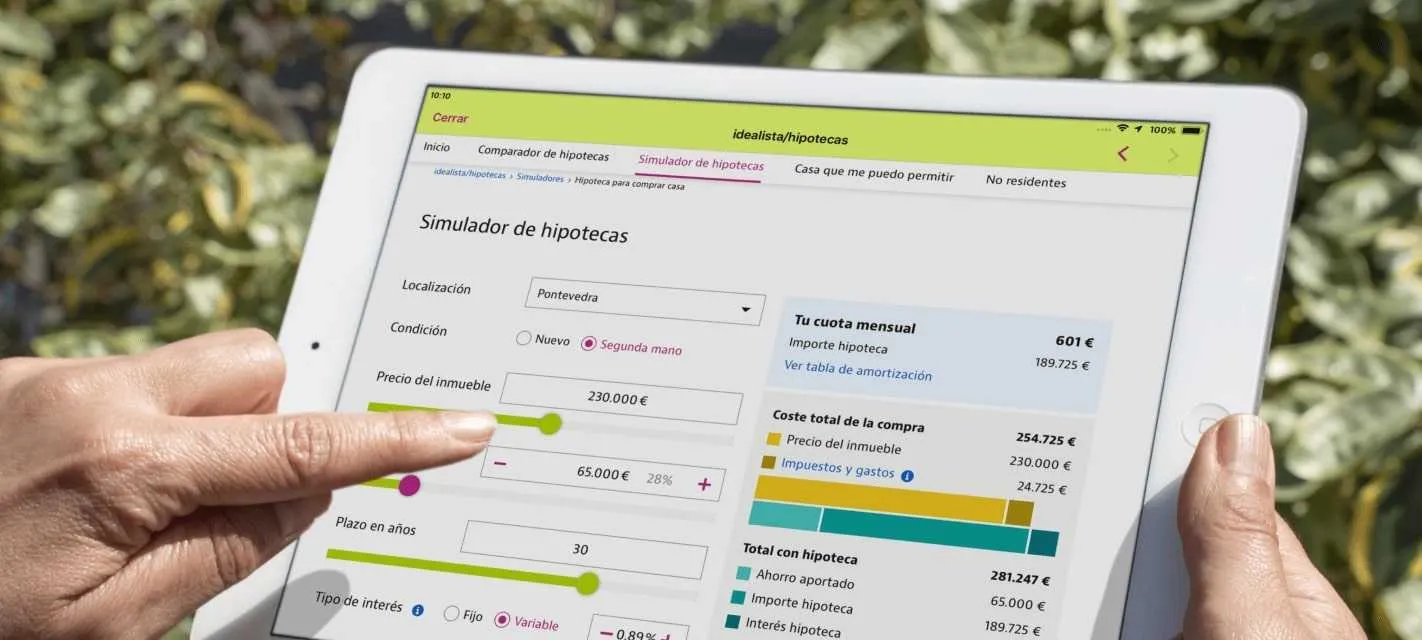

Start with Mortgage Pre-Approval: Define Your Budget

When buying with a mortgage in Portugal, the first step is typically not property viewing, but obtaining a mortgage pre-approval.

You will need to submit basic documentation such as your tax number (NIF), proof of income, bank statements, and your intended purchase budget. Based on this information, the bank will provide a pre-approval indicating your estimated borrowing capacity, interest rate range, and expected monthly payments.

Although pre-approval is not a final loan approval, it helps you clearly define your budget and avoids the risk of selecting a property that cannot be financed. Completing this step early is key to an efficient process.

Property Search: The Market Moves Quickly

Once your budget is defined, the next step is to begin searching for a property.

One distinctive feature of the Portuguese market is that buyers typically do not pay agent fees, making it common to work with real estate agents. Property turnover can be fast, especially in cities like Lisbon and Porto, where competitively priced properties often attract multiple buyers at the same time.

This means that beyond simply viewing properties, timely decision-making is essential.

Signing the CPCV: Securing the Property

After selecting a property and agreeing on a price with the seller, the next step is to sign the CPCV (Promissory Contract of Purchase and Sale) and pay a deposit, usually around 10% of the purchase price.

This stage effectively “reserves” the property and creates a legally binding commitment for both parties to proceed with the transaction. It also marks the point at which the bank begins the formal mortgage approval process.

Formal Bank Approval: The Most Critical Stage

Following the CPCV, the bank proceeds with the formal mortgage approval.

This includes a property valuation, a detailed review of the borrower’s financial profile, and confirmation of the loan terms. During this stage, you may be required to provide additional documentation and sign financing agreements.

Typically, the period between signing the CPCV and completing the transaction ranges from 30 to 60 days, depending on the speed of the bank’s approval and the completeness of the documentation.

Completion (Escritura): Finalizing Ownership

Once the mortgage is approved, the process moves to the final stage — the completion (Escritura).

At the notary office, the buyer, seller, bank representative, and legal advisors come together to finalize the transaction. This includes settlement of the purchase price, property registration, and the establishment of the mortgage.

At this point, the transaction is completed, and you officially become the legal owner of the property.

Summary: Preparation and Timing Are Key

Overall, the mortgage purchase process in Portugal can be summarized as a clear sequence:

Pre-Approval → Property Search → CPCV → Bank Approval → Completion

The process itself is not complicated, but success largely depends on preparation and timing. The earlier you define your financing capacity, the clearer your options become. The more complete your documentation, the smoother and faster the process will be.